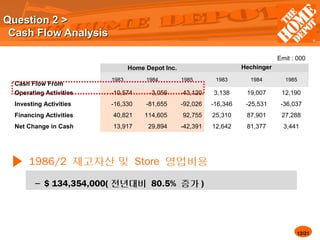

In terms of to order a home, the conventional faith try you to an effective 20% downpayment try needed. Yet not, saving upwards anywhere near this much are tough, particularly for earliest-big date homeowners otherwise individuals trying to go into today’s housing marketplace easily. And here individual home loan insurance policies (PMI) will come in, providing an alternative getting individuals who don’t features a large down fee.

What’s private home loan insurance policies, and just why must i worry?

While you are like most People in america, you truly need to borrow funds to purchase property. And if you’re and then make a down payment out-of lower than 20%, the lender must manage alone. Individual home loan insurance coverage (PMI) is insurance rates that positives the lending company because of the protecting all of them but if your default in your future mortgage repayments. But how is it possible you, the target homebuyer, take advantage of using up personal financial insurance rates?

By paying a month-to-month PMI premium, you can secure a mortgage and go into the housing marketplace ultimately than should you have to go to to keep right up getting a beneficial full 20% down-payment. What’s more, it enables one start building house security and you may take advantage of the great things about homeownership instantaneously.

Focusing on how PMI functions

While you are PMI allows consumers to get in the brand online personal loans Montana new housing market that have an effective lower down payment, there’s a disadvantage. For a while, you have some high month-to-month mortgage payments because you will be borrowing from the bank a lot more initial. not, quite often, PMI will not remain in perception for your mortgage term. Once your collateral home has reached 20%, you could request so you’re able to terminate PMI.

One which just love a house otherwise decide on home financing, it is essential to speak with your loan manager regarding the PMI will set you back according to your unique finances. It’s equally important to understand the factors you to determine how much you’ll be able to pay money for PMI.

Situations which affect PMI will cost you

- Brand of home:Whether you’re to invest in a single-house, condo otherwise townhouse impacts your own PMI rates.

- Kind of loan: Conventional financing and you can government-backed funds has more PMI standards.

- Loan identity:Are you gonna be a beneficial fifteen-year otherwise 29-12 months financial?

- Credit score: A top credit rating generally speaking results in all the way down PMI superior.

- Interest: This impacts your overall mortgage payment, along with PMI premium.

- Down payment count: The more you devote down initial, the lower the PMI.

- Loan-to-worth (LTV) ratio: A lesser LTV basically leads to less PMI payments.

- PMI type of:Different types of PMI provides differing will cost you and formations.

Your own PMI fee try determined considering multiple situations. On average, PMI can cost you between 0.5% in order to dos% of your own amount borrowed per year. Such as, for folks who use $450,000, within a beneficial PMI rates of just one%, you would shell out $4,five hundred annually or just around $375 monthly. Keep in mind this really is a quote, along with your genuine cost hinges on the loan count, PMI rates or any other points. To locate a crisper idea of your own PMI rates, play with the home loan calculator to see how some other mortgage wide variety, rates and PMI prices might apply to your own monthly premiums.

Prominent types of PMI

There are different kinds of private financial insurance rates. Deciding on the best choice for you depends on your personal needs and you can house-buying problem.

- Borrower-paid off mortgage insurance rates (BPMI): You only pay this premium inside your monthly homeloan payment. When you visited 20% equity, you could potentially consult in order to cancel BPMI.

Are you willing to prevent paying PMI?

How you can avoid PMI is to try to generate a beneficial 20% down payment. not, that’s not constantly feasible. Particular authorities-supported loans, for example FHA finance and you may Virtual assistant money, keeps built-during the PMI or insurance premiums. For those who opt for a loan with PMI, select one with cancellable terms, to help you remove PMI once your collateral reaches 20%.

To remove PMI, you’ll want to consult they in writing, as well as your lender get qualification standards, such as for example although not limited by:

You want More and more PMI?

Individual mortgage insurance rates assists homeowners secure financing with a smaller deposit, but it is important to comprehend the types, will set you back and you can choice. If you are happy to learn more about PMI or explore their home loan options, contact a movement Home loan manager now.

Note: Path Mortgage is not connected, recommended, or sponsored of the Department off Pros Issues otherwise Government Housing Administration and other authorities department.